VIP Days

Interested in GBSC? Be our guest at VIP Day!

VIP Days

Interested in GBSC? Be our guest at VIP Day!

Programs & news

Affordable

Ranked #1

We are the most affordable Bible college in America with ABHE & regional accreditation.*

Tuition, fees & aid

Don’t pay full price. Find the general costs of college, your specific costs and learn how financial aid works.

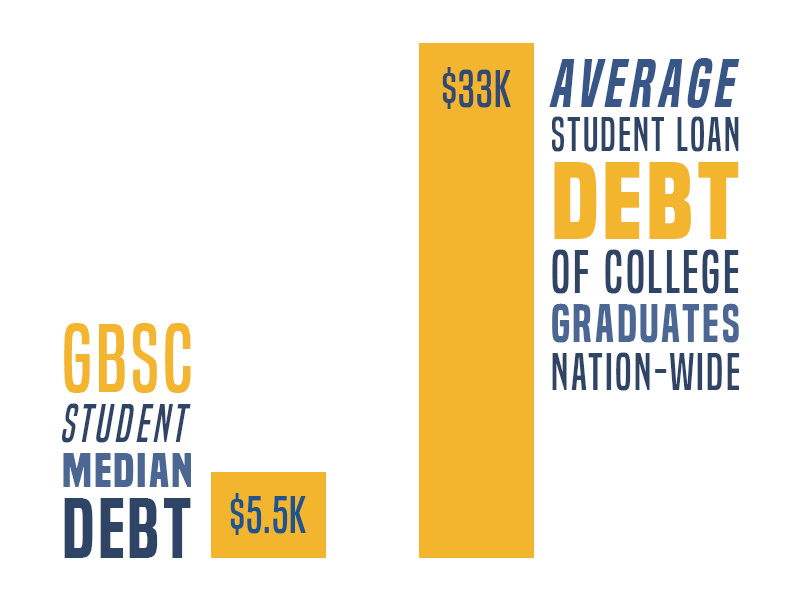

Less debt is better

Find out how and why we keep our costs down so you can focus on the things that matter.

Transformative

Transformation happens here all the time. Watch Cameron’s story unfold.

“I wanted to hear the best argument that the holiness movement had to offer. At GBS, God really taught me how to love him.”

Spiritual life at GBSC is important. Watch Darnell’s story unfold.

“The time I spent at GBS was a period of intense and painful transformation. But the pain now lives in the shadow of a much greater joy.“

Brennan’s life was transformed, how will yours? Watch Brennan’s story unfold.

“When I graduated from high school I wanted to have my own construction company. I hadn’t even considered going to a Bible college.“

Degree options

Campus degrees

Develop your craft, discover your calling. Start your adventure today.

Online degrees

Pursue your college education on your own time and from wherever you like.

Masters degrees

Craftsmanship takes time. So, pursue your advanced degree on your timeframe.

Pathways

Pre-approved paths to success.